This Market Update is written by our Capital Market specialists each week to bring you insight into what's happening in the market and how it may affect mortgage rates and real estate trends.

Market Commentary:

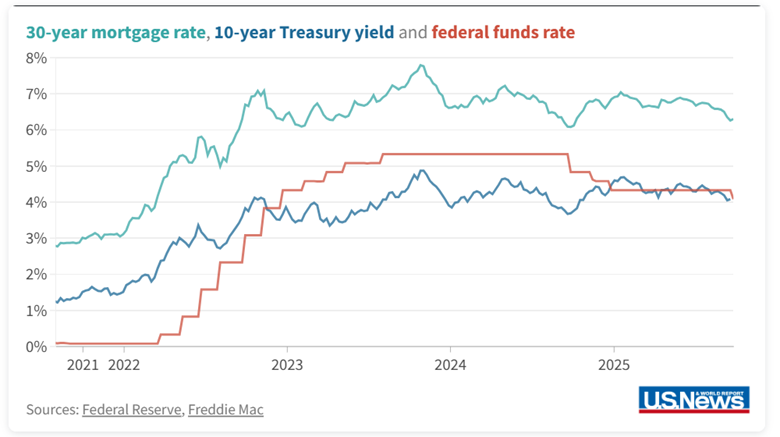

Mortgage rates saw modest movement this week, offering a mixed bag for borrowers. The average 30-year fixed rate edged down to 6.37%, while the 15-year fixed held steady around 5.75%. Jumbo and FHA loans remain competitive, with rates hovering near 6.24% and 6.19%,respectively.

Markets are closely watching the Federal Reserve’s tone as inflation data continues to cool. Fed Chair Jerome Powell hinted at the possibility of rate cuts before year-end, though the central bank remains cautious. The next FOMC meeting in late October will be pivotal for rate trajectory expectations.

Inventory remains tight in many markets, but buyer activity is picking up slightly as rates stabilize. First-time homebuyers are showing renewed interest, especially in suburban and secondary markets where affordability is more favorable.

Should you wait to buy until mortgage rates go down?

In short, no. You probably shouldn’t wait to buy a home until mortgage rates drop more drastically. Mortgage rates are just one part of the affordability equation. You also have to consider home prices, a factor of housing supply and demand.

The current housing market is in a crunch. To put it simply, buyers outnumber homes for sale, especially homes in price ranges accessible to the first-time home buyer. When supply and demand are out of balance like this, home prices tend to remain high since sellers know they’ll have multiple buyers interested.

According to data from the Federal Reserve Bank of St. Louis, the median sale price of single-family homes has generally trended upward since Q1 of 2009. At that time, the median sale price was $208,400. The median price had risen to $410,800 by Q2 2025.

Fed Watch: Target rate (in bps) possibilities, according to the CMEGroup (as of 10/16/2025 – 12:00 PM EST):

This Is the Best Time To Buy a Home in Every Metro—as Peak Buying Season Approaches

The 2025 Affordability Bowl: First-Time Buyers Face 4th-and-Long, But the Game Isn’t Over:

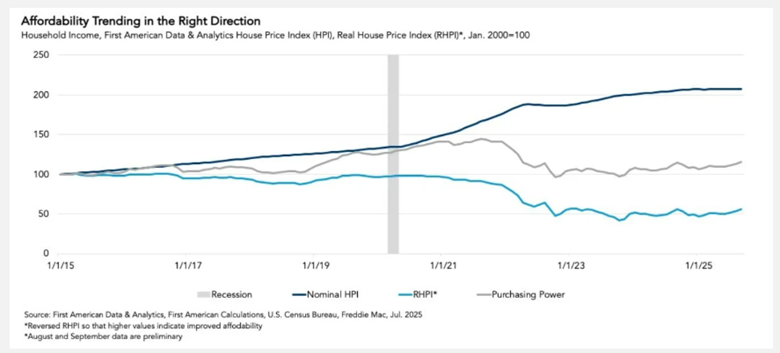

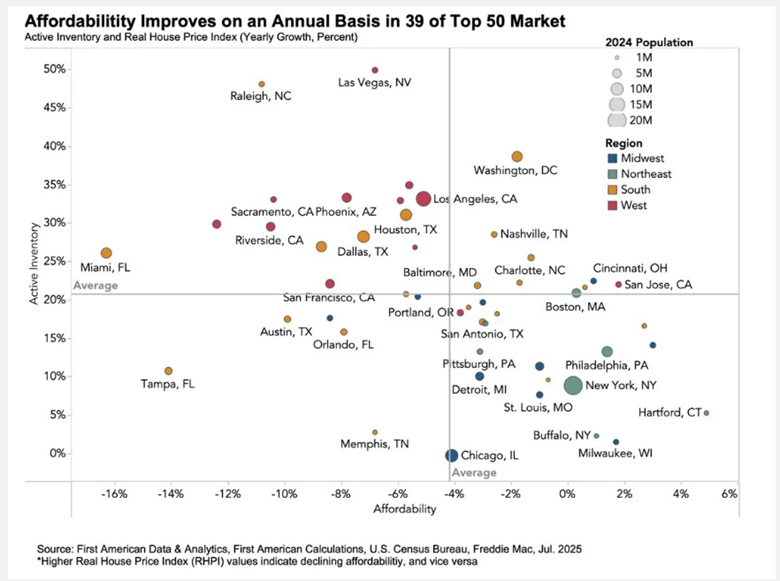

Affordability Improves for Fifth Straight Month, Offering a Glimmer of Hope for the Housing Market

25Q3 bank earnings were a stunning $50 billion, up 20% Y-o-Y! All divisions did well, including wealth management, lending, trading and M&A/investment banking, suggesting a healthy economy. But not so fast. The drivers were big firm borrowing for M&A, and affluent households borrowing against booming equity values. Middle-class deposits grew, but Main Street borrowing and household credit card growth were minimal. The wealthiest households and biggest firms are driving results. - Elliot F. Eisenberg the Bowtie Economist

News You Can Use:

· Major real estate developers are fast becoming power brokers

· Fed Governor Waller sees more rate cuts but says central bank needs to be 'cautious about it'

· Real Estate Agents Agree: This Home Feature Attracts Buyers Instantly

· US Housing Market Falling Into ‘Deflationary Vortex,’ Analyst Warns - Newsweek

· Home sales to jump nearly 10% in 2026, forecasters say

· Fed warms to rate cuts, but labor risks could hurt home sales

· Zillow Group, Inc. - Zillow's 2026 home trends: Color-drenched, whimsical and resilient

*Communication is intended for Industry Professionals only and not intended for Consumer Distribution

Interest rate and annual percentage rate (APR) are based on current market conditions as of 10/16/2025, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by HomeServices Lending, LLC. Not available in all states. Rate is as of 10/16/2025 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac’s economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac’s business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an “as is” basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.

.png)