This Market Update is written by our Capital Market specialists each week to bring you insight into what's happening in the market and how it may affect mortgage rates and real estate trends.

Market Commentary:

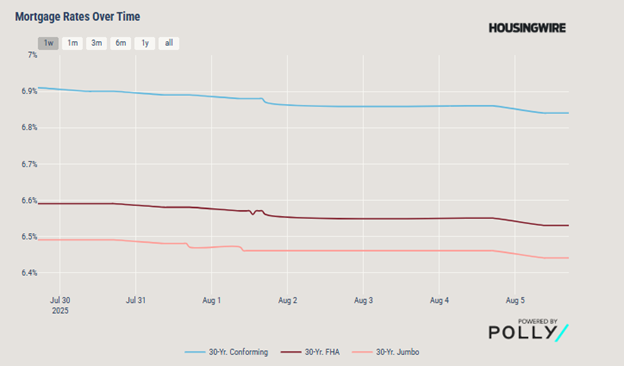

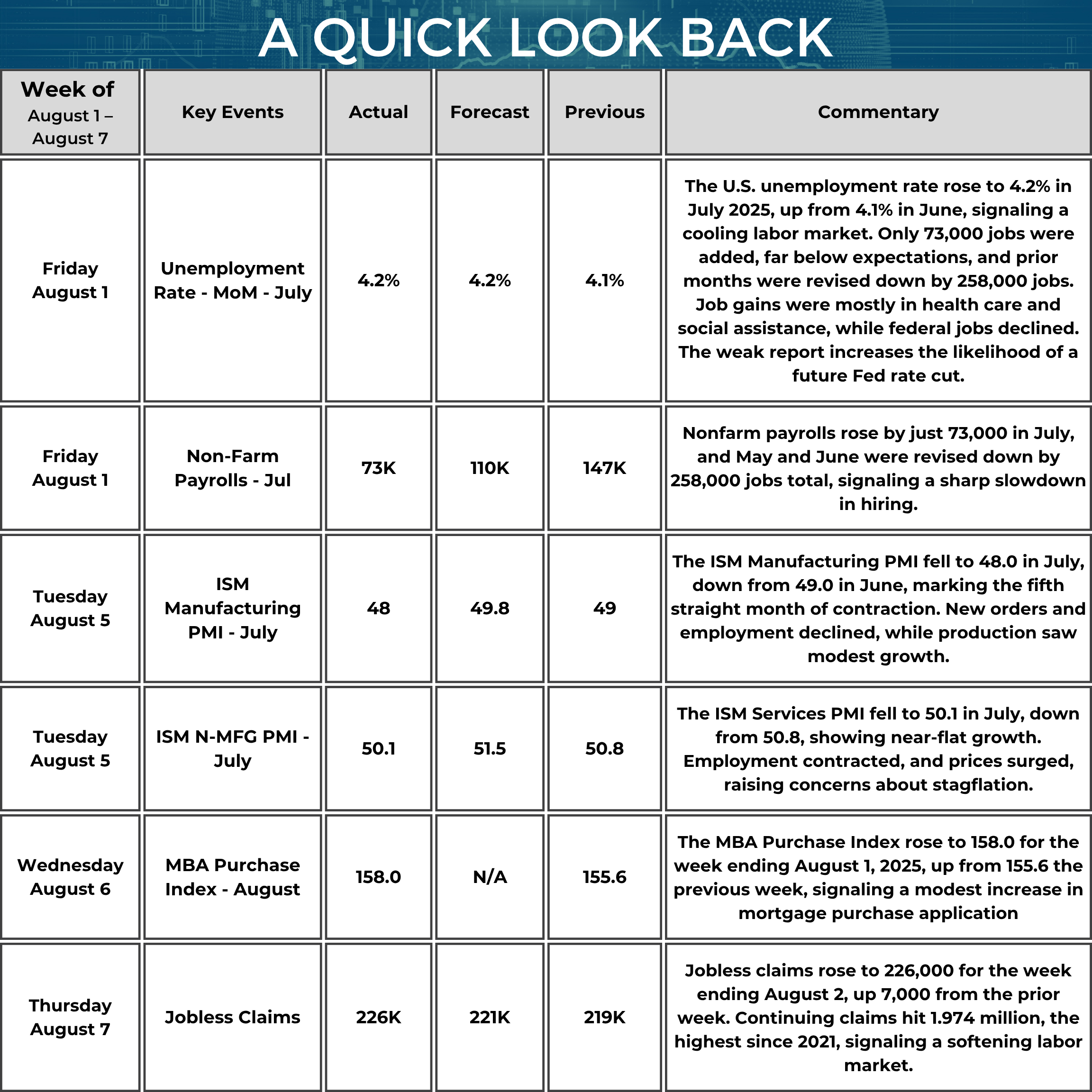

As of August 1, 2025, mortgage rates have declined to the upper mid-6% range, marking the lowest levels of the year. The drop followed disappointing July nonfarm payrolls, which came in at just +73,000, alongside major downward revisions to prior months totaling -258,000. The unemployment rate held steady at 4.2%, but soft labor market momentum signaled slowing economic growth. The ISM Manufacturing PMI fell to 48.0, remaining in contraction, while the Services PMI barely held in expansion at 50.1, with hiring shrinking in both sectors. These indicators have pushed Treasury yields lower, which directly translated into more favorable mortgage rates.

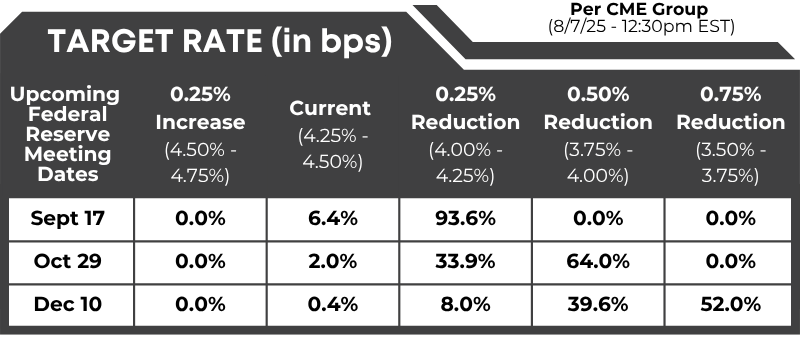

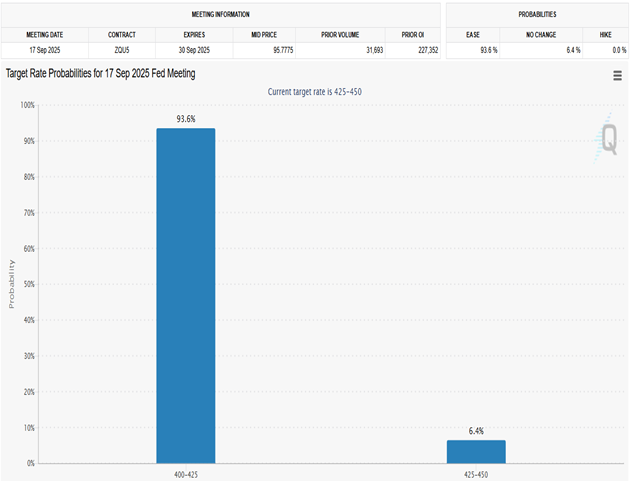

Markets are now pricing in a 93.6% chance of a Fed rate cut in September, reflecting increased recession concerns. The MBA Purchase Index for early August hasn’t shown a strong rebound yet, but falling rates could support demand. Housing affordability remains a key constraint, but easing rates may open opportunities for sidelined buyers. Overall, the mortgage market is in a mild easing phase, driven by softer data and shifting policy expectations.

The trend now points toward gradually declining rates, though volatility remains tied to upcoming Fed actions.

Fed Watch: Target rate (in bps) possibilities, according to the CME Group (as of 08/07/2025 – 12:00 PM EST):

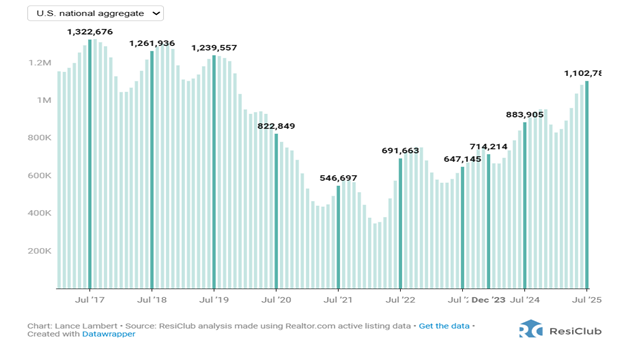

Active Homes for Sale Inventory from July2017-July 2025 plus forecasts through 2027

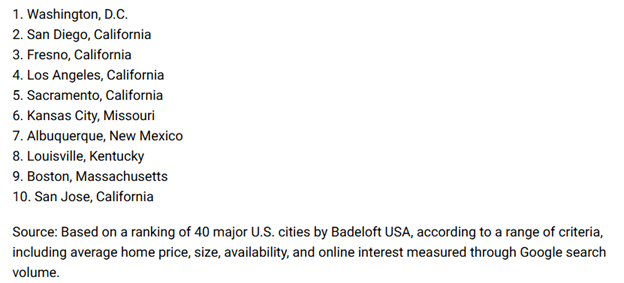

10 Most Desirable Major U.S. Cities for Home Ownership

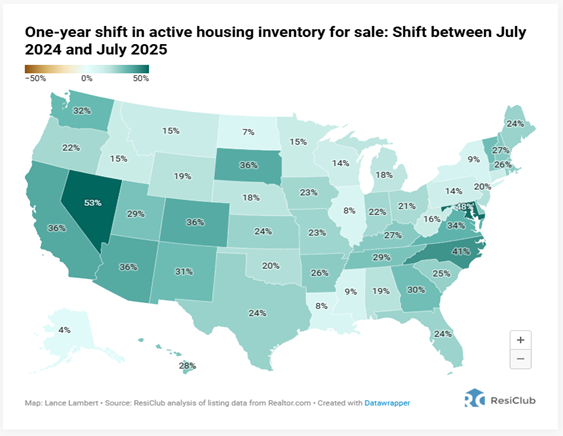

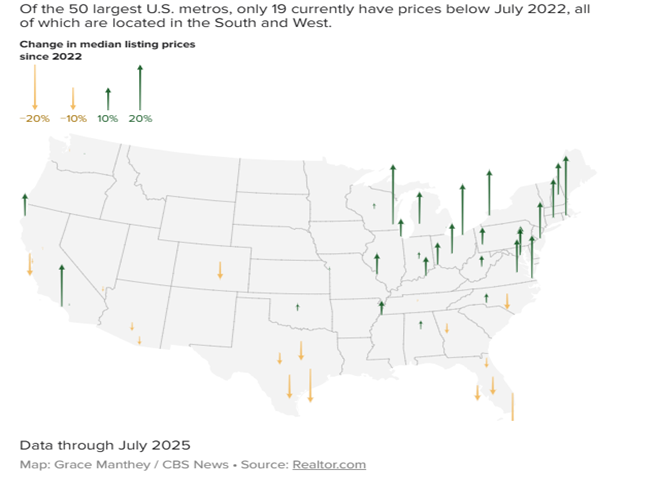

Home prices are dropping in some regions of the U.S. but rising in others. Here’s where.

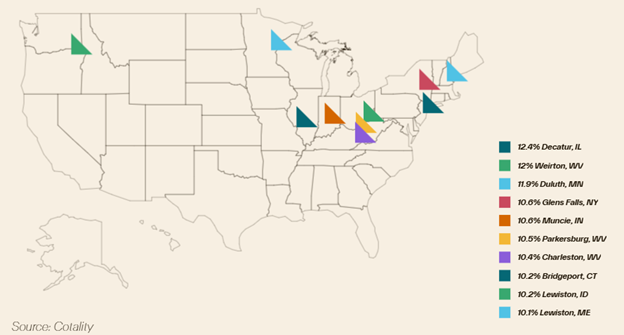

Top 10 Hottest Markets

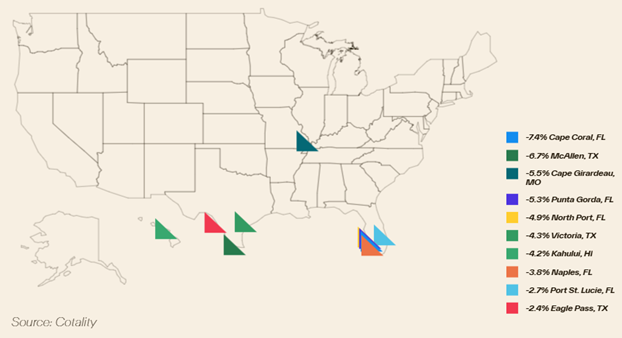

Top 10 Coolest Markets

Troubling Termination

The only reason employment data revisions are noticeably larger is due entirely to low response rates by surveyed businesses. Pre-Covid, response rates on the initial survey were 80%, now they’re below 60%. By the third wave, response rates are where they were pre-Covid, 94%. Lower response rates mean larger standard errors, and larger eventual revisions. Rather than shooting the messenger, fine firms who refuse to quickly respond to the survey.

News You Can Use:

• Mortgage rates plunge to 10-month low, opening window of opportunity for house hunters

• Bank of America CEO: Our Economists believe there will not be a recession

• Fed President Kashkari of MN possibly sees 2 rate cuts as reasonable for 2025

• U.S. added just 73,000 jobs in July and numbers for prior months were revised much lower

• Map Shows States Where Homeowners Benefit Most from Capital Gains Tax Plan

• Trade Deficit Decreased to $60.2 Billion in June

• Where Home Prices are rising and where declining in the US

• Map Shows Most-Desirable Major US Cities for Home Ownership

*Communication is intended for Industry Professionals only and not intended for Consumer Distribution

Interest rate and annual percentage rate(APR) are based on current market conditions as of 08/07/2025, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by HomeServices Lending, LLC. Not available in all states. Rate is as of 08/07/2025 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac’s economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac’s business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an “as is” basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.

.png)