This Market Update is written by our Capital Market specialists each week to bring you insight into what's happening in the market and how it may affect mortgage rates and real estate trends.

Market Commentary

Interest rates for the week of May 22nd to ay 29th remained flat. Interest rates aren’t going anywhere—maybe. Minutes from a meeting of the Federal Reserve Bank leaders, which was held in early May and released on May 29, show the central bank voted to undertake open market operations “as necessary” to maintain the federal funds rate in a target range of 4.2% to 4.50%. In a related action, the Board of Governors of the Federal Reserve System voted unanimously in early May to approve the establishment of the primary credit rate at the existing level of 4.5% – which means interest rates for lenders, consumers and the rest of Americans won’t be budging in the near term, much to the dismay of the Trump administration.

The Federal Reserve has a dual mandate to target low inflation and unemployment. It can raise interest rates to slow inflation, but that can cause unemployment. Or it can cut rates to boost job growth, but that can cause inflation. The information available at the time of the May meeting indicated that consumer price inflation remained somewhat elevated.

Given so much economic uncertainty, the Federal Reserve is adopting a wait-and-see approach when it comes to interest rate adjustments. After cutting borrowing costs three times last year, the central bank has held rates steady so far in 2025, extending its holding pattern for a third consecutive meeting on May 7.

Fed Watch: Target rate (in bps) possibilities, according to the CME Group(as of 05/30/2025 – 12:00 PM EST):

Market Review: Optimal Blue's Production Metrics:

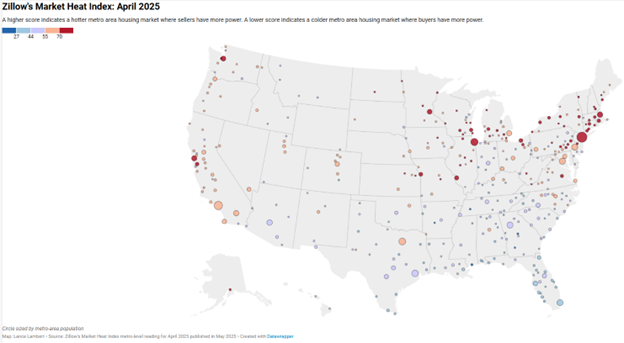

Zillow's Market Heat Index: April 2025

Bonds

The 10-year Treasury term premium is up 60bps since early April and is 100bps above its past decade norm. The rise isn’t due to expectations of faster growth, nor rising inflation expectations, the usual culprits behind rising rates. The rising term premium is due to massive trade/tariff uncertainty and expectations of a widening in the already irresponsibly large budget deficit. This will largely negate any stimulus from tax cuts.

- Elliot F. Eisenberg, Ph.D., Economist

News You Can Use

- May 2025 Economic and Housing Outlook - Fannie Mae

- Fed worried it could face ‘difficult tradeoffs’ if tariffs reaggravate inflation, minutes show

- Consumer confidence for May was much stronger than expected on optimism for trade deals

- S&P Corelogic Case-Shiller Index Records 3.4% Annual Gain in March 2025

- Mortgage rates rose to the highest level since January, but demand from homebuyers still grew. Here’s why

- Volatile Spring Selling Season Continues

Interest rate and annual percentage rate (APR) are based on current market conditions as of 05/29/2025, are for informational purposes only, are subject to change without notice and may be subject to pricing add-ons related to property type, loan amount, loan-to-value, credit score and other variables. Estimated closing costs used in the APR calculation are assumed to be paid by the borrower at closing. If the closing costs are financed, the loan, APR and payment amounts will be higher. Contact us for details. Additional loan programs may be available. Accuracy is not guaranteed, and all products may not be available in all borrower's geographical areas and are based on their individual situation. This is not a credit decision or a commitment to lend. actual interest rate, APR, and payment may vary based on the specific terms of the loan selected, verification of information, your credit history, the location and type of property, and other factors as determined by HomeServices Lending, LLC. Not available in all states. Rate is as of 05/29/2025 and is subject to change at any time without notice. Opinions, estimates, forecasts, and other views contained in this document are those of Freddie Mac's economists and other researchers, do not necessarily represent the views of Freddie Mac or its management, and should not be construed as indicating Freddie Mac's business prospects or expected results. Although the authors attempt to provide reliable, useful information, they do not guarantee that the information or other content in this document is accurate, current, or suitable for any particular purpose. All content is subject to change without notice. All content is provided on an "as is" basis, with no warranties of any kind whatsoever. Information from this document may be used with proper attribution.

.png)